Finance Minister Nirmala Sitharaman tabled the Income Tax bill in parliament on February 13. This bill is expected to cut through the jargon in the 1961 Income Tax Act, making it easier to understand for the common people. However, this bill aims to modernise and streamline India’s long-standing direct taxation system by simplifying tax provisions and establishing a straightforward legal framework. This provision will come into effect by April 1, 2026.

The Modi government has maintained the structure and core principles of this bill closely to the current Income Tax Act. In this bill, FM introduced major changes to make it easier for people, adding only 622 pages instead of 880 pages, with 536 sections higher than 298 sections of the current Income Tax Act, 1961, 23 chapters, and 16 schedules.

Changes take in the Income Tax Bill.

Replacing a six-decade-old act in the budget session, the finance minister stated that this bill ensured the S.I.M.P.L.E. core principle for people to follow and enforce. These five core values are defined as “streamlined structure and language, integrated and concise, minimising litigation, practicing and being transparent, learning and adapting, and efficient tax reforms. However, heading towards budget implementation next year, the government took significant steps in this proposed law, including:

Tax year and no assessment year

Taking a major step to make this bill easier for people, the term “previous year” as mentioned in the recent tax act was replaced with “tax year.” The tax year is outlined in section 3 of the new bill, stating that the financial year will continue to start on April 1 and end on March 31. The recent ongoing act states that income earned in the previous year (say 2023-24) is paid in the assessment year (say 2024-25). While this concept has been removed from the upcoming act.

No Alteration in Tax Rates and Slabs

The recently passed bill does not claim any adjustment in tax slabs and rates that are relevant to the taxpayers. The primary goal of this bill is to simplify the structure of income tax laws. But a change has been made in this budget session that up to 12 lakh-earning employees are free from these tax slabs.

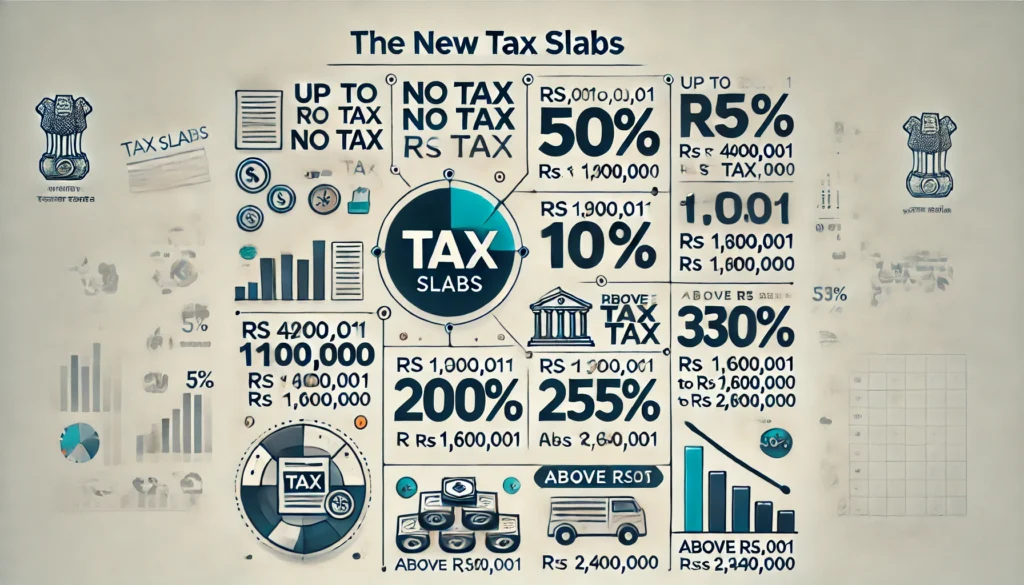

Tax Slabs Under New Tax Regime

Up to Rs 400,000: No tax to be levied.

From Rs 400,001 to Rs 800,000: The tax rate is 5%.

From Rs 800,001 to Rs 1,200,000: The tax rate is 10%.

From Rs 1,200,001 to Rs 1,600,000: The tax rate is 15%.

From Rs 1,600,001 to Rs 2,000,000: The tax rate is 20%.

From Rs 2,000,001 to Rs 2,400,000: The tax rate is 25%.

Above Rs 2,400,000: The tax rate is 30%.

No Changes in Salary Heads

There is no such change made in the salary head. Under the next tax bill, the income subject to taxation is categorised in several categories, including wages, annuity or pension, Gratuity, fees or commission, perquisites, profits in lieu of, or in addition to, any salary or wages, Advance salary, leave encashment, contribution to provident fund beyond the tax-free limit, contribution by central government or any other employer to employee’s pension scheme accounts, and contribution by central government to the agniveer corpus. It was hoped that the government would make some changes, but despite expectations of changes, the new bill will remain as earlier.

Consolidation of TDS/TCS provisions under one single section

In this bill, Nirmala Sitharaman suggests that the implementation of tax deduction has been made on a variety of income sources, including salaries, professional fees, interest income, rent, and more. According to sources, TCS (Tax Collected at Source) will be enforced on specific transactions, including the sale of alcohol, tendu leaves, minerals, and scrap materials (1%-5%); the sale of motor vehicles above Rs 10 lakh (1%); and foreign remittances exceeding Rs 7 lakh (5%).

In this proposed law, anyone who fails to follow TDS/TCS regulations will be penalised as defaulting for neglecting to deduct or pay TDS/TCS, as well as incurring a monthly interest charge of 1% on outstanding TDS/TCS amounts.

There are several sections pertaining to tax deduction at source (TDS), such as 194A (interest), 194I (rent), 194J (professional fees, fees for technical services, royalty payments), 194H (commission), 194C (contracts), etc. While most sections have similar provisions, the differences lie in the applicable tax rates and thresholds.

To streamline and simplify the TDS provisions (excluding salaries), the Income Tax Board (ITB) has consolidated these provisions under section 393 of the ITB in a concise and tabular format.

TDS on salaries as outlined in section 192 of the Income Tax Act is now detailed in section 392 of the ITB. Similarly, the provisions of Tax Collected at Source (TCS) under section 206C of the Income Tax Act are conveniently presented in a tabular format in section 394 of the ITB for easy reference.

Presumptive taxation regime

The proposed bill revises the presumptive taxation regime (Sections 44AD, 44AE, and 44ADA), raising turnover limits to ₹5 crore for businesses and ₹75 lakh for professionals. It also simplifies TDS and TCS provisions with separate reference tables for residents, non-residents, and non-deduction cases.

Ahead of its presentation in Rajya Sabha, this bill is successfully presented in the Lok Sabha. However, some members of the opposition staged a walkout, and others lobbed fierce questions at the finance minister. Commenting on her, the Congress party member, Manish Tewari, said that this bill is more complicated than the older one. Trinamool MP Saugata Roy criticised the new bill as being “mechanical.”